ServiceNow:

ServiceNow is available to service your portfolio.

Today I am going to present to you a SaaS company which is revolutionizing how work is done in the workplace. I have owned shares of this company since 2018 and have added last week. Obviously I am not going to tell you or recommend you that you should buy this company. But I am very excited about his company’s future and particularly I got very impressed with new CEO Bill McDermott. He was previously CEO of SAP. His life story itself is very inspiring and if you have 25 minutes time to spare this YouTube video is truly inspiring. Bill Mcdermott

If you really like my work or write up, please don’t hesitate to retweet or like, it will motivate me to write more and reach wider audience.

Company profile

ServiceNow is a platform built in the cloud that has a framework with tools to build applications.

It is the platform of platforms of workflow.

Company states in its 10K its “purpose is to make the world of work, work better for people.”

It achieves this by organizing workflows on a single enterprise cloud platform called the Now Platform.

It has built the best SaaS solution for IT service Management (ITSM). It commands 40% market share in TISM. It is executing a land and expand strategy. It has expand its offering from ITSM to ITOM (IT operation management) that includes HR operation, and customer service

It is the first SaaS company to reach 5 B revenue growth organically!

Products

The Now Platform

Standardized applications specifically designed for automating IT, Employee and Customer workflows.

The graph below summarizes the function and services ServiceNow offers:

Market size and opportunity:

Digital transformation in the next 3 years will be an 8 trillion market. The space NOW is playing at is around 175 B market opportunity. The company asserts itself as a control tower of digital transformation. Current revenue of the company is around 5 Billion and I see a long run of growth still untapped. The company itself has been growing revenue at an average > 30% for the last 5 years.

Watch NOW CEO explain the opportunity

Financials

Financial: Source, www.koyfin.com

The company is growing at 30% with 78% gross margin and has free cash flow margin of greater than 30%. I haven’t heard of any company which is growing at that scale with that free cash flow margin organically!

Looking at the balance sheet; it has 3.4 B in cash and 1.6 B in long term debt. It has 3.1 billion in shareholder equity.

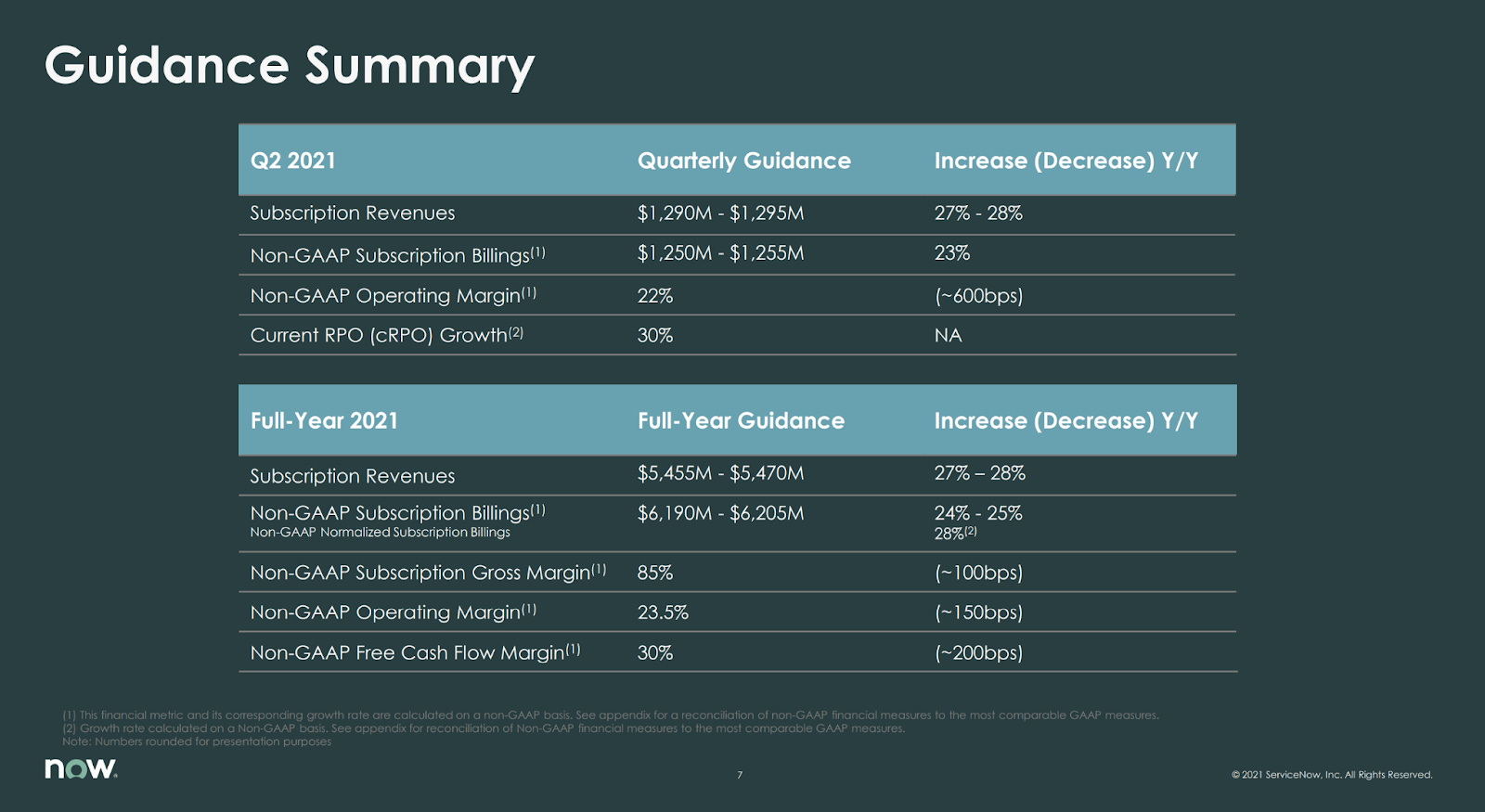

Guidance

The company organized virtual investor day on May 10, 2021. It updated its road map of hitting revenue of 10 B in 2024 and 16 billion by 2026 all organically!

Multiples

Source: www.koyfin.com

The company of NOW size, moat and growth should be trading around 20 times EV/Sales multiple.

If it hits its guidance of 16 B in 2026 and it trades around 20 times revenue = 320 B in 5 years; it is trading around 90 B; it will give us 28% CAGR!

But if some argues that it should be trading at lower multiples of 15, that will give us 21% CAGR and if trades at 10 times revenue multiple = 12% CAGR!

I have copied and pasted important metrics from company’s investor presentation:

Guidance for next Quarter and Full Year 2021

Non-Gaap Gross Margins

Non-GAAP operating and free cash flow margin

Close price 6/10/2021 = 489.

Disclaimer:

The stocks mentioned in my newsletter are not intended to be a list of buy recommendations but rather some ideas for your watchlist. Perhaps they end up in your own portfolio after you conduct your own research and due diligence. Some of the stocks mentioned in my newsletters have smaller market capitalizations and therefore can be more volatile. I always encourage and strongly recommend everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizing in accordance with your own risk tolerance, risk profile and investment objectives.

I can trade in and out of the securities mentioned in my newsletter at any time with or without any reasons and without any updates.