Making sense of Yield Curve, GDP growth, M2 supply and Feds action

Making sense of Yield Curve, GDP growth, M2 supply and Feds action

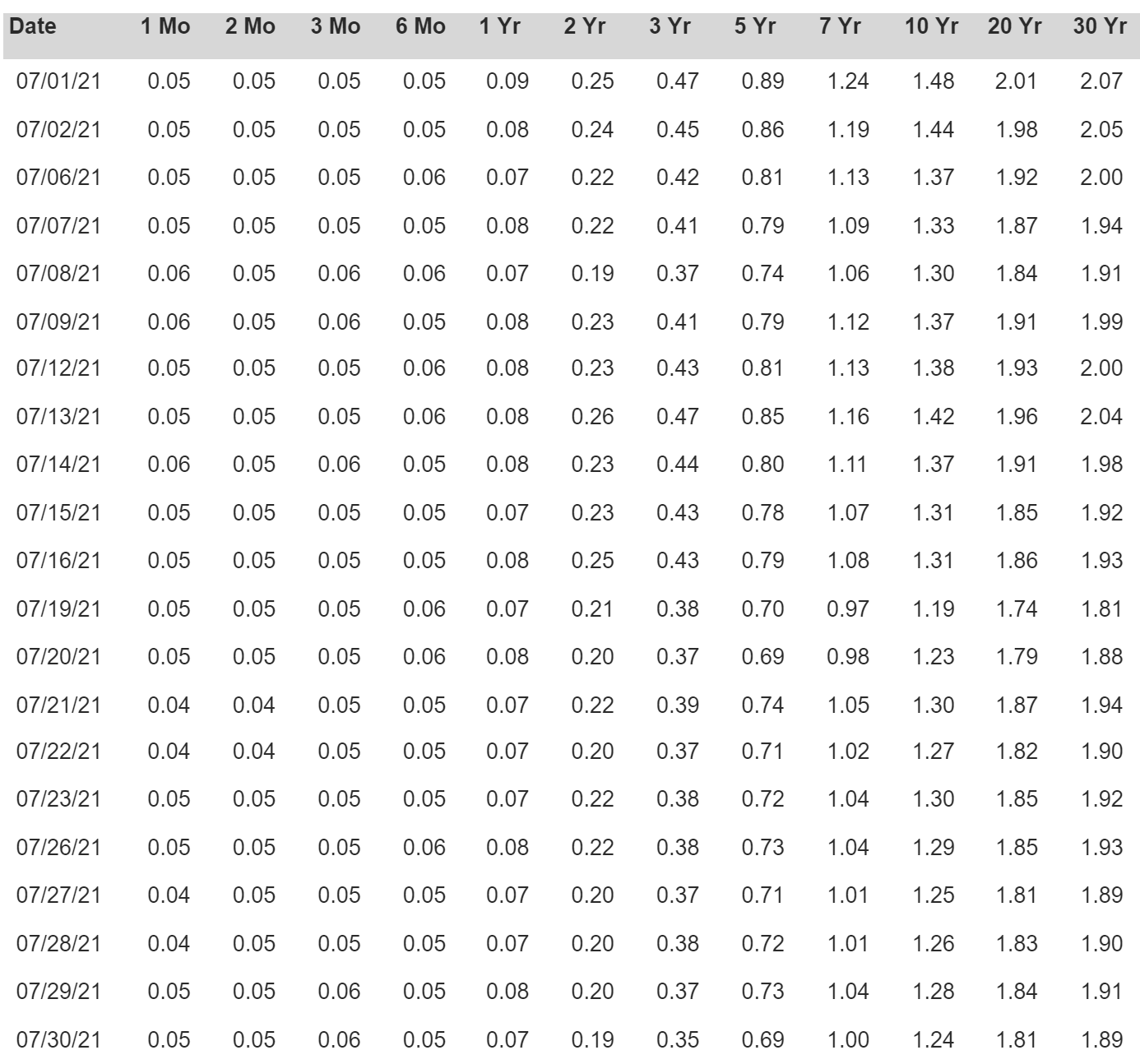

Below is the table of the yield curve from US Treasury website:

The yields are falling faster at the long end of the curve than on the short end. This means that despite current inflation fear, quantitative easing, bond investors are forecasting tepid growth and low inflation. When the equity market and bond market have diverging views, usually the bond market is right.

It is natural to wonder why there is no inflation despite the government spending trillions of dollars and the Federal reserve creating money out of thin air and to expect runaway inflation.

Recently I came across the writings and research of Dr. Lacy Hunt (Economic Overview (hoisington.com) who regularly pens quarterly views and outlook on the economy which I find very informative. I encourage readers to go to his website and read every quarterly report. In his 2nd quarterly review and outlook (2018) he explains the relationship between money velocity (V) and US recessions.

Money Velocity (V) = GDP/ M2 or GDP = V * M2

M2 = cash, checking deposits and easily convertible near money.

And

GDP = C + I + G + X where

C = Consumption

I = Investment

G = Government spending

X = Net exports

After reading his outlook on this topic, I came to realize that most of the developed countries are trying to inflate GDP by more government spending via government debt. Each time more debt is issued, the lesser the impact of the debt on generation of GDP. “If the debt produces a sustaining income stream to repay principal and interest, then velocity will rise since GDP will eventually increase beyond the initial borrowing. If advancing debt produces increasingly smaller gains in GDP, then velocity falls.”

Let's first see what determines GDP.

Productivity (GDP) is measured as the ratio of output to input.

P = Output/Input,

Output is function of input:

Capital (Debt capital + Equity capital)

Labor

Natural resources

Technology

The optimal interaction of these four factors results in GDP growth.

Human labor interacts with capital, natural resources and technology to produce goods and services which in turn increases GDP.

One can easily deduce that increasing only one factor of production ( capital) will not cause increased productivity. One can have unlimited supply of capital but if there is not proportionate increase in labor, natural resources and technology to interact, the productivity and output can’t be increased.

Labor capital in the western countries is declining due to an aging population. Equity capital comes from personal (13.6%) saving which is dismal. Technology will change faster and make us more efficient and negatively impact human capital due to creative destruction.

Only tool left with the government is issuing government debt (Debt capital) to increase GDP or growth or create demand. Since government debt or spending is used for consumption and not investment, the GDP generating capacity of debt is diminishing. Debt will create growth in GDP and hence increase is money velocity only if debt is used for productive activity where income is generated to satisfy principal and interest payment.

Now lets see what is happening to M2 velocity which is an important determinant of inflation along with M2 base.

M2 velocity (V) is defined as a ratio of nominal GDP to a measure of the money supply, M2 ( V = GDP/M2). Increasing V is forerunner of inflation while decreasing V is forerunner of deflation.

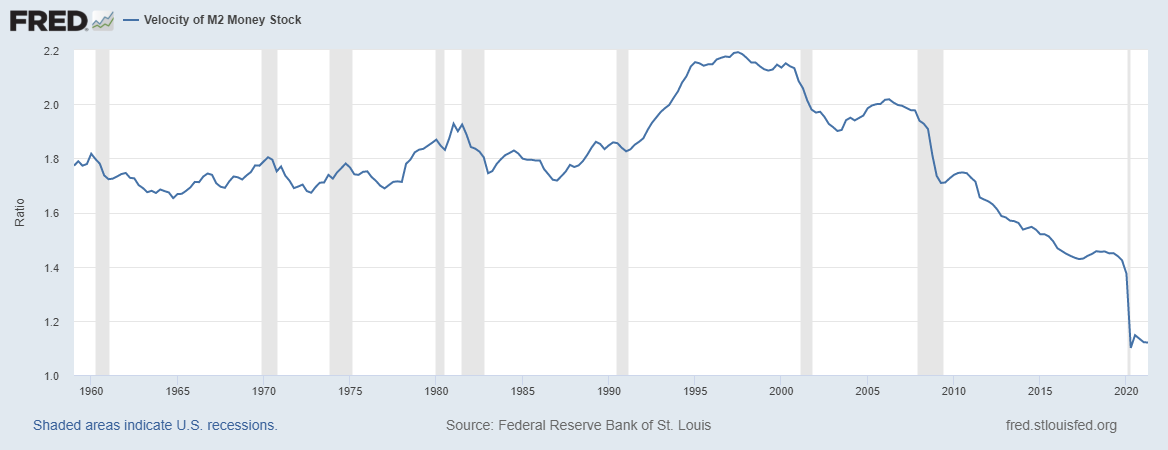

Lets see what is happening to Velocity of M2 in the chart published by St Louis Federal Reserve 3 days ago below:

As you have noticed the V declined sharply in March 2020 reaching 1.1, picked up a little bit Q3 2020 to 1.4 and is in declining trend in Q2 2021 to 1.12.

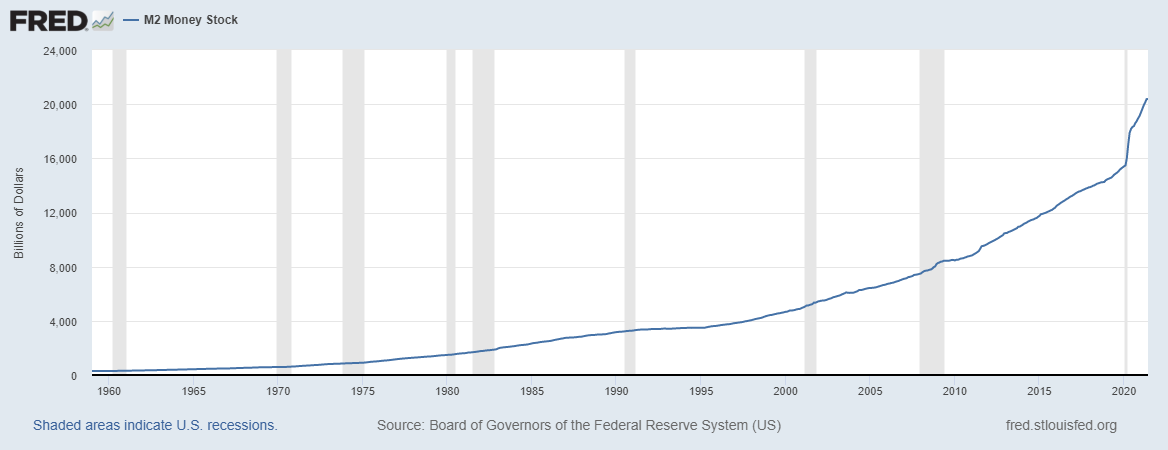

While many in the street is focused on this graph of M2 which is going up

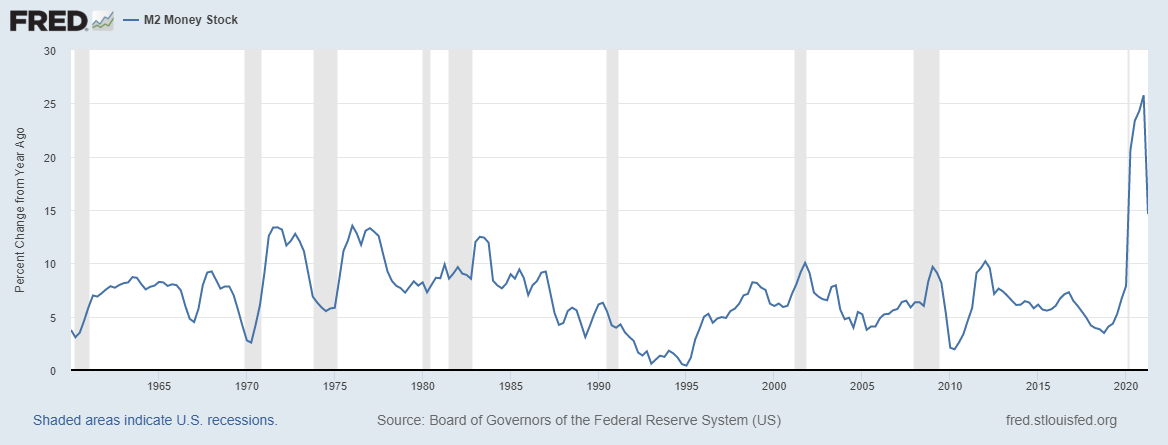

But if we look at annual percentage change of M2 Money stock, it is declining in Q2, 2021

In summary, I see that M2 velocity (V) is declining, rate of change of M2 stock base is declining, which are two factors in our equation of GDP = V*M2 suggests that the economy is slowing down. I wouldn’t be surprised to see the Fed delaying tapering and postponing the federal funds rate hike for the foreseeable future until broad measures of money supply and money velocity changes. However, one should note that stock market corrections and crashes may not reflect what is happening in the underlying economy and this article is no way prediction about where the stock market is headed in near or long term.

This article is for educational purposes and it is purely my personal quest of understanding the economy, GDP, growth and inflation.

Thanks for writing this article. Much appreciated. Definitely makes things easier for me understand what is going on with fiscal policy.

thanks for sharing.