AppLovin

This company riding secular trend of mobile-gaming may not remain under-valued!

AppLovin

AppLovin (APP) is a mobile application technology company that is riding the secular trend of

mobile-gaming. It provides advanced tools for mobile app developers to grow their business by automating and optimizing the marketing and monetization of their apps.

The company estimates that it has a total market opportunity of $189B in 2020 which is expected to grow at 10.6% CAGR, up to $283B in 2024.

Mobile app developers lack access to marketing, monetization, and data analytics tools required

to compete in a competitive market of more than 4.8 million apps available on the

Apple App Store and Google Play Store. AppLovin provides toolsets for app developers to

market their product and monetize it.

Both organic growth, as well as strategic acquisitions happen to be their growth strategy.

The company has

AppLovin Core Technologies: This consists of AXON machine learning recommendation engine, App Graph data management layer, and elastic cloud infrastructure.

AppLovin software: This is a suite of tools for developers to get their mobile apps discovered and downloaded by the right users, optimize returns on marketing spend, and maximize monetization of engagement.

AppDiscovery is a marketing software solution.

Max is the in-app bidding software

Compass is an analytics software tool within Max that gives developers testing capabilities, insights, and intelligence.

The company’s moat lies on the flywheel effect of its products. The AppLovin software’s scaled distribution, first party content, and core technologies’ recommendation engine creates a powerful flywheel effect that reinforces each component and improves the company’s position and capabilities.

Source: Company’s 10K

The company asserts strategic acquisitions and partnership as one of its strategies and has acquired MAX Advertising systems Inc, SafeDK Mobile Ltd, and PeopleFun and has forged partnership with Belka Games.

Let's see if the company is growing profitably or not.

Based on the above analysis, the company is scaling. Revenue is growing faster than expenses. We can see that the revenue is growing at 123% year over year quarter and 10.78% consecutive quarter while the expenses growth was 111.6% year over year quarter and 5% growth in consecutive quarters. Looking at the balance sheet, it has a debt of $1.7 B with total non-current liabilities of $1.9 B while total current assets of $1.7 billion out of which $1.1 B is cash and cash equivalents.

Let's look at a recent quarterly earnings report:

Software revenue grew over +200% organically Y/Y and +40% Q/Q

Revenue grew +123% Y/Y to $669 million, organic growth increased +97% Y/Y

Business Software Platform revenue grew +256% Y/Y to $146 million

Achieved record Software Platform Enterprise Clients (SPEC) at 366

GAAP Net Income improved to $14 million from a net loss of $22 million, with a GAAP net margin of 2%

Adjusted EBITDA grew 202% Y/Y to $184 million and adjusted EBITDA margin improved to 27%

Guidance for 2021:

Revenue of $2.65 to $2.7 B (80% year over year growth)

Adjusted EBITDA of $680-700 million

Competitive Landscape

It is a very crowded space. When the total addressable market is huge, it is natural to have multiple players and multiple players can win. It is comforting to know that the founder is at the helm and the largest individual shareholder. Again, no investment is risk proof, but I am willing to bet alongside founder CEO Adam faroughi. It is noteworthy that he started this company in 2012 and in the short span of a decade it has a $2.6 B revenue run rate!

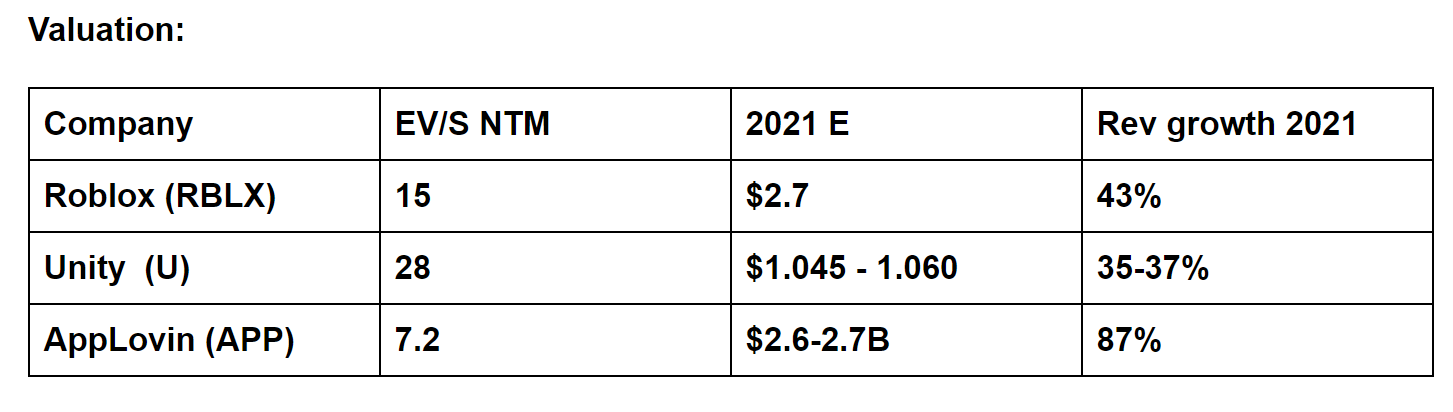

I find this valuation attractive. I find all three companies to be great companies. However, AppLovin appears to be more attractively priced and it may not remain undervalued to its peers any longer. Obviously, the value of the company is never calculated just on a 4X3 table, this is just a short-hand guide. The valuation of a company or business has both qualitative and quantitative factors interacting with return on invested capital, growth and competitive position in the field of business.

Adam Foroughi has 94% approval rating on Glassdoor review. I listened to a number of YouTube interviews on Adam and he comes out as humble, pragmatic CEO who rewards his employees based on performance/talent than on pedigree. It is also comforting to know that the CEO is the largest individual shareholder who bought the stock in the open market at around 60 dollars last quarter.

I just felt that it is too good to pass up this opportunity. I started a starter position at $61/share.

Hi Anil, why do you think market is undervaluing this company, is there something that we are missing, is it because its not a SAAS business? When I find an undervalued business many times there are issues that market prices in. Sometime market is wrong, which is good time to buy companies but its important to ensure we are not missing anything. I will also look into this company in more details. Good pick. --Pranshu

Hi Anil, thanks for sharing your picks and along with a brief summary of your thoughts. Other than flywheel effect do you see any moat? What are some of the main competitors and in the absence of any intellectual property, I was wondering other companies/competitors can develop this tool relatively easily (I am not a technologist, so I could be wrong). I would appreciate if you could add more color and deep dive to the moat and uniqueness of this company compared to others which protects its from competition. Thanks